Domain-Specific LLM Benchmarks Guide: The 2026 Map of Vertical AI Evaluations

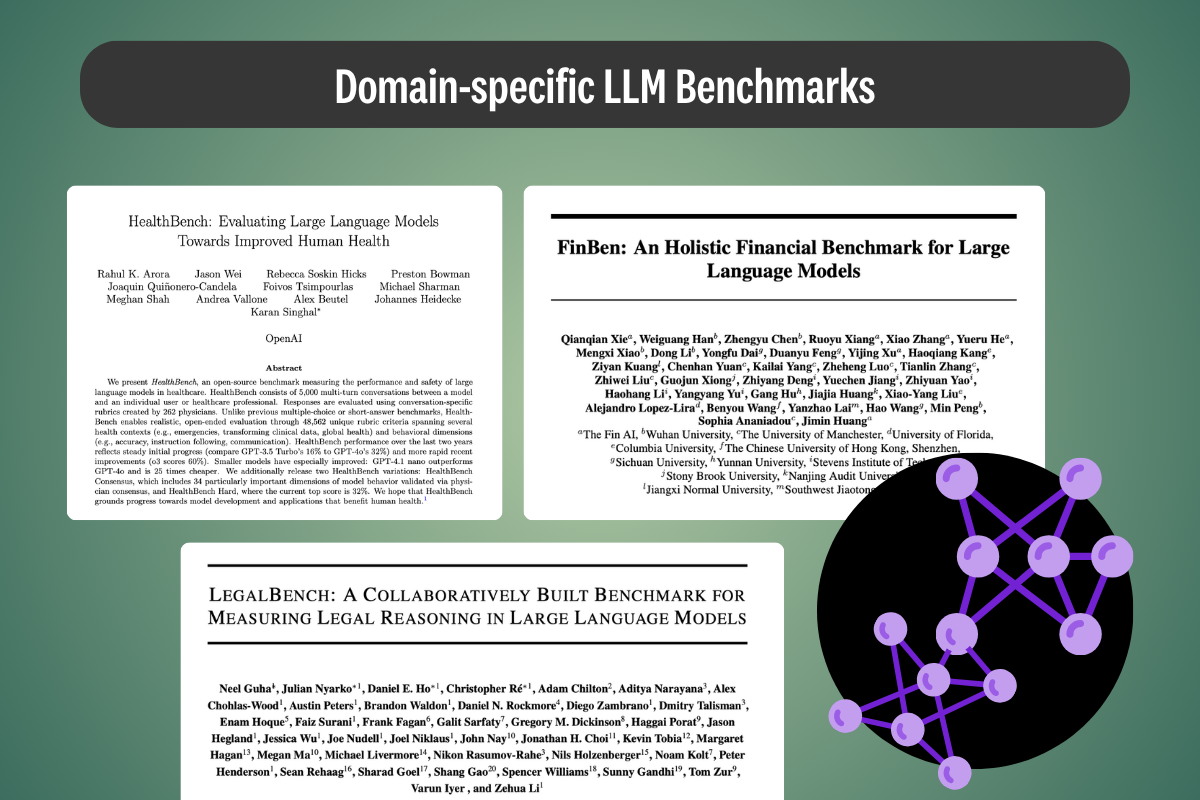

General-purpose AI benchmarks have saturated, and the field has fragmented into open-source vertical evaluations for domain specific knowledge like medicine, law, finance, science, code, cybersecurity, multilingual reasoning, and multimodal expert work. This guide maps the major public domain-specific LLM benchmarks in 2026, explains how they are built, and shows why even the strongest of them still leave production teams exposed without expert human review.

.png)

![Best On-Premise Data Labeling Platforms for Regulated Industries [2026] Guide](https://cdn.prod.website-files.com/68da32b2041c593b0511a582/6a574849a90d08dc8b9b547d_Competitor%20Article%20-%20Listicle%201%20(2).webp)

![8 Best Data Labeling Platforms for Large-Scale Annotation [2026]](https://cdn.prod.website-files.com/68da32b2041c593b0511a582/6a340ef16e870a66feb5fe71_1.webp)